Seed As An Asset Class

Venture Capital (VC) has long been associated with outsized risk and reward with some investors hesitant or unable to participate. The hesitance has left opportunities available for those aware of the merits of VC as an asset class as it has outperformed over a long-run period, reaching new recent highs.

With growing awareness, VC has garnered increasing investment over time. Further, classes within the space with distinct attributes have been defined - Seed (pre-product market fit), Early Stage (product market fit), and Later Stage & Growth (developing to scale) - that provide the ability to invest in specific stages of the market with the best managers. Of these, we believe in Seed and the opportunities that the asset class provides for funds equipped to participate in the earliest stages of company development.

Here is why:

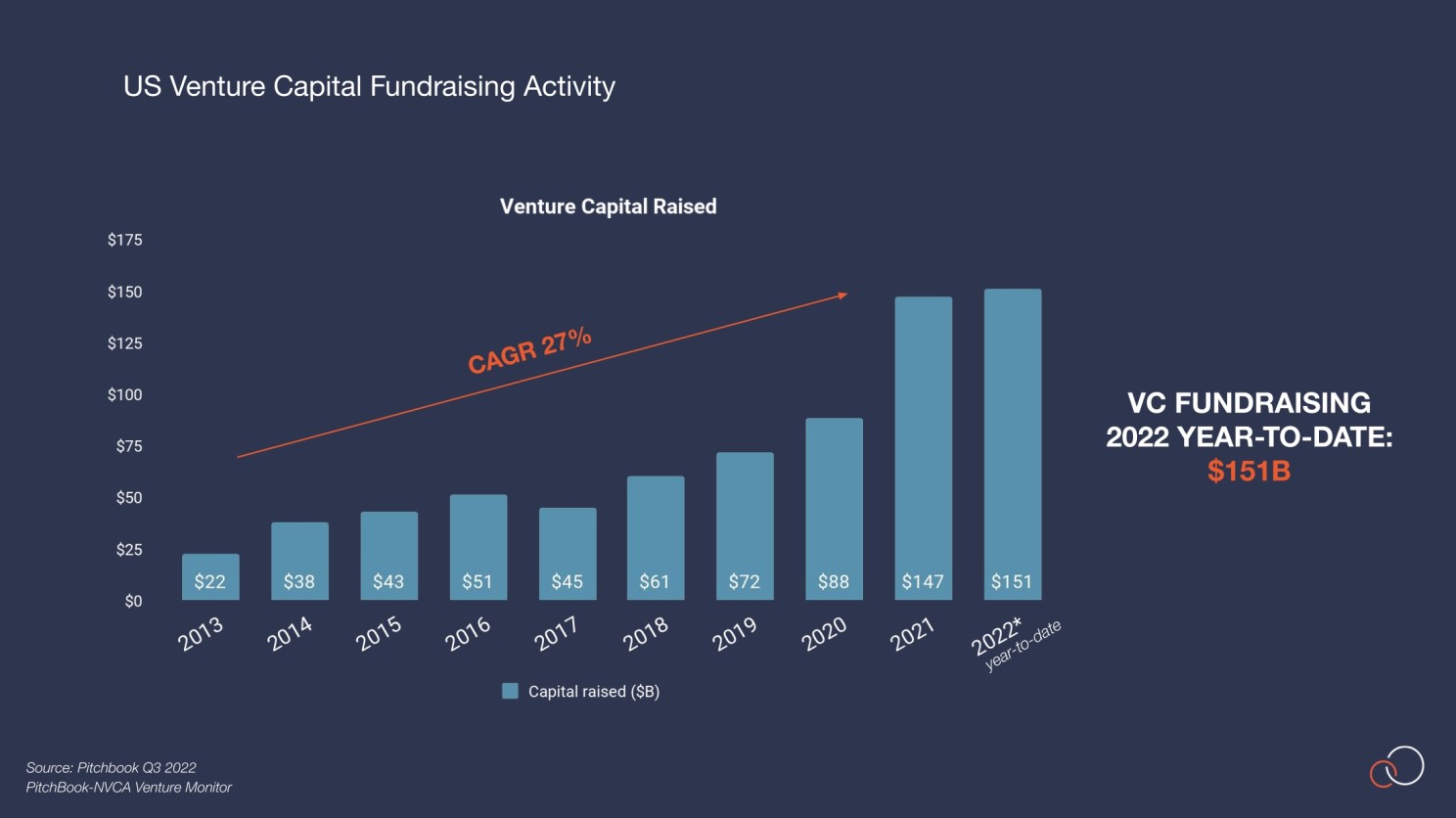

There’s Money In Venture Capital. A Lot Of It

VC fundraising has had solid long-term momentum. Over the last 10 years, fundraising has grown over 27% Year-over-Year (YoY), reaching a high water mark in 2021 of $147B. That amount has already been exceeded through the first three quarters of 2022, reaching $151B, and it is on pace for a meaningfully higher record for the year. This is all despite market turmoil and a pullback in later-stage VC and Growth. We are likely at the pinnacle, at least for now, as fundraising that commenced before volatility built-up earlier this year is captured in recent activity and a slowdown or plateau can be expected before any renewed growth.

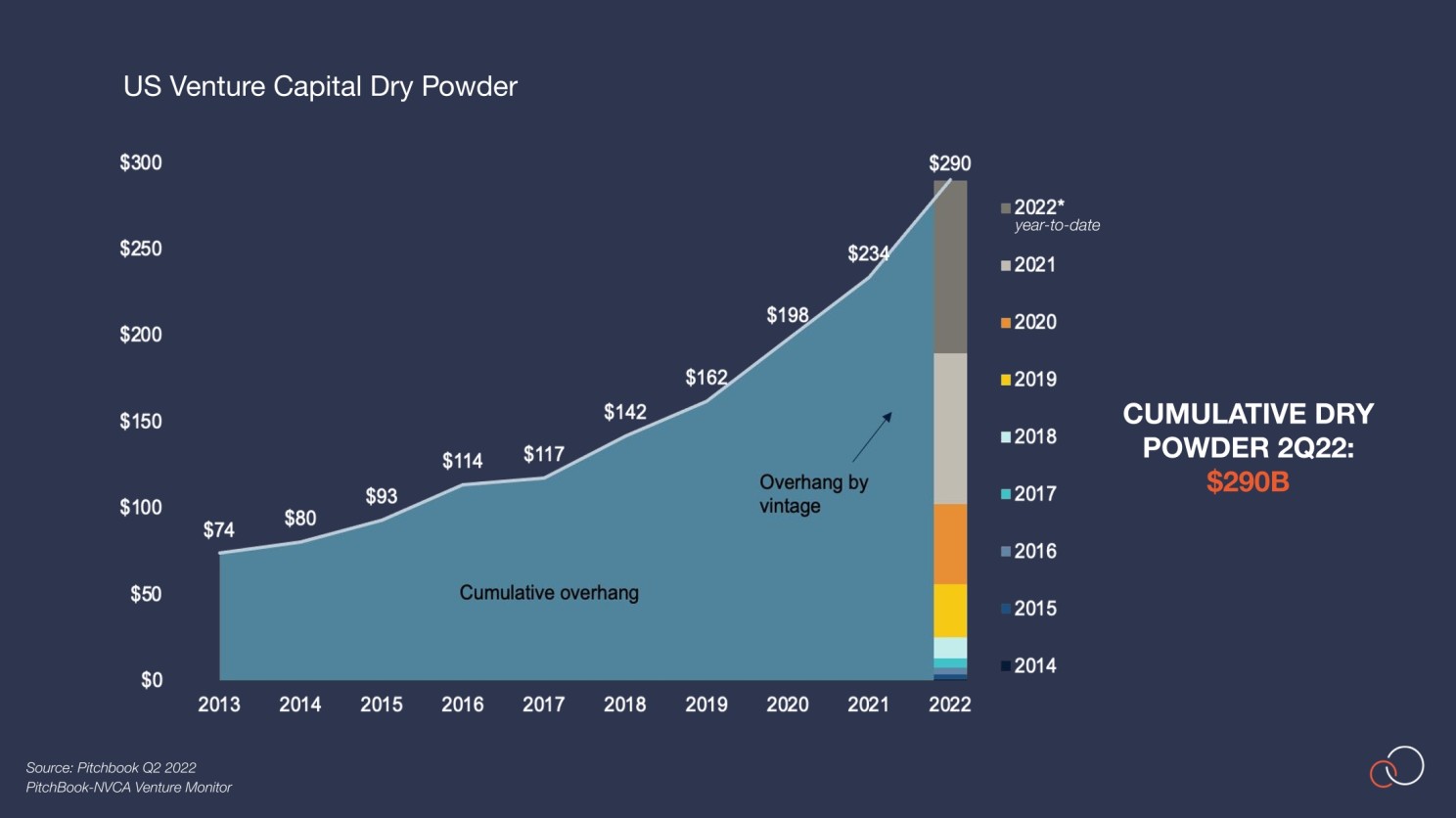

Dry Powder Is Available for Great Companies

Coupled with record fundraising, there has been significant continued accumulation and deployment of capital over time. On the accumulation side, dry powder grew to about $290B at the end of the second quarter, driven predominantly by pending deployment of recent fund vintages, from 2019 through 2022.

This capital will be invested over time as fund managers won't just sit on the sidelines – they're actively looking for opportunities to drive LP returns and will be cognizant of the timelines for each of their funds.

Available capital will ensure continued investment in new technologies and will benefit VC overall. In particular, this will include Seed and subsequent early stage follow-on, where activity and valuations have remained relatively resilient. Deals may take longer and will require more thoroughness in diligence, but the best companies will get funded.

On the deployment side, there was a run-up in investment from 2017 to 2021 (PitchBook 2022). Deals from a volume perspective grew at a 12% YoY rate, but at the same time the value of deals expanded at a much faster pace of 40%. This reflects the sizable run-up in round-sizes and valuations experienced over the last few years, where invested capital upsized quickly, especially in later-stage VC. With the uncertainty flowing through the markets this year, an impact is finally being seen in deal activity as we get deeper into 2022.

Seed Activity Has Been Resilient

While deal volume (# of deals) has been relatively steady, deal value ($'s in deals) and valuations are experiencing increased pressure, especially in later-stage. For the second quarter of 2022, deal value declined about 14% YoY, while deal volume has maintained levels, growing marginally at about 3%. Initial estimates for the third quarter show a much sharper decline in deal value and a moderate decline in deal volume.

It’s important to note, however, that much of these declines are contained within later-stage VC. Within Seed, deal value grew 18% and deal volume increased marginally for the second quarter and both were relatively stable in the third quarter based on initial estimates. We do expect Seed activity to experience some impact – and create opportunities – but Seed is more insulated from the markets as an Asset class given the long-term investment perspective and expected time horizon to liquidity. The bottom line – Founders in Seed will still get funding for the most innovative ideas. Investments in Seed are reflective of where industries can move to with the development and adoption of new technologies, further unshackling markets from current conditions.

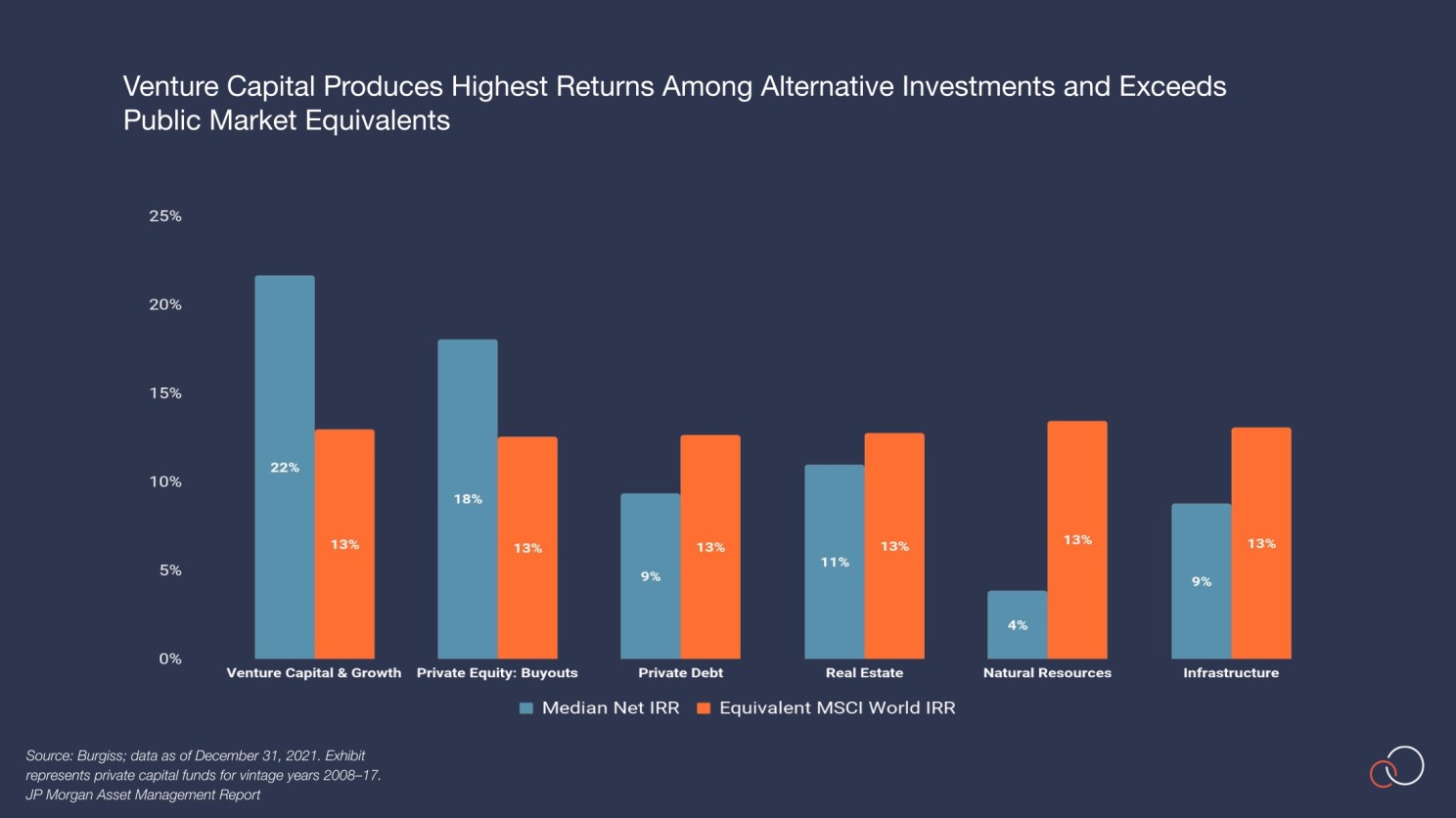

VC Generates Outsized Returns

Capital flowing into VC is drawn by the attractiveness of the returns from the asset class relative to public markets and other private market alternatives. Over a long-run period of 10 years:

- Venture and private equity (PE) have outperformed the public markets

- VC and PE have out-indexed other alternative asset classes

- VC in particular has delivered an additional 9% in returns relative to public market equivalents (e.g., MSCI indexed portfolio), outpacing PE and other alternative investment classes

These historial returns have drawn attention to the space as investors seek greater yield and are willing to take on long term holds to achieve them. They are looking to VC – specifically good managers, who are able to make the right picks and help set their portfolio companies on paths to grow and scale.

Within VC, Seed Outperforms

Relative to later-stage VC, Seed funds have historically delivered greater median returns from both a TVPI and IRR perspective. There is also a greater dispersion among these returns, where high decile Seed fund managers deliver even higher performance relative to their peers in later-stage. Recognizing these managers and what differentiates them can accrue meaningful upside to investors.

This is what we know more than ever about Seed as an asset class:

- Seed has outperformed over time and will continue to deliver

- Valuations have not run up at the same level as other VC classes, creating moderate entry points where positions can be secured with meaningful ownership at the lowest valuations in a company’s life cycle

- Seed provides the opportunity to partner with Founders to set companies up with solid foundations, where operating expertise is a valuable tool to drive impact

- Seed enables investing at the leading edge of innovation with opportunities that can transform markets

To outperform in Seed, managers need to identify the right founding teams with the vision and complement of abilities to build and scale transformational companies. Oceans is uniquely levered towards operating expertise to find the right opportunities and enable Founders to build teams and deliver on the promise of their companies.

Within Seed, we're not investing for the markets as they stand today. We're investing for the markets as we believe they will be in the future.

Subscribe to get updates from our founders and things we’re thinking about.